The COVID-19 pandemic and ensuing global economic crisis have shaken up the fintech industry, forcing many to readjust their strategies and expand their revenue streams on the back of a contracted funding environment.

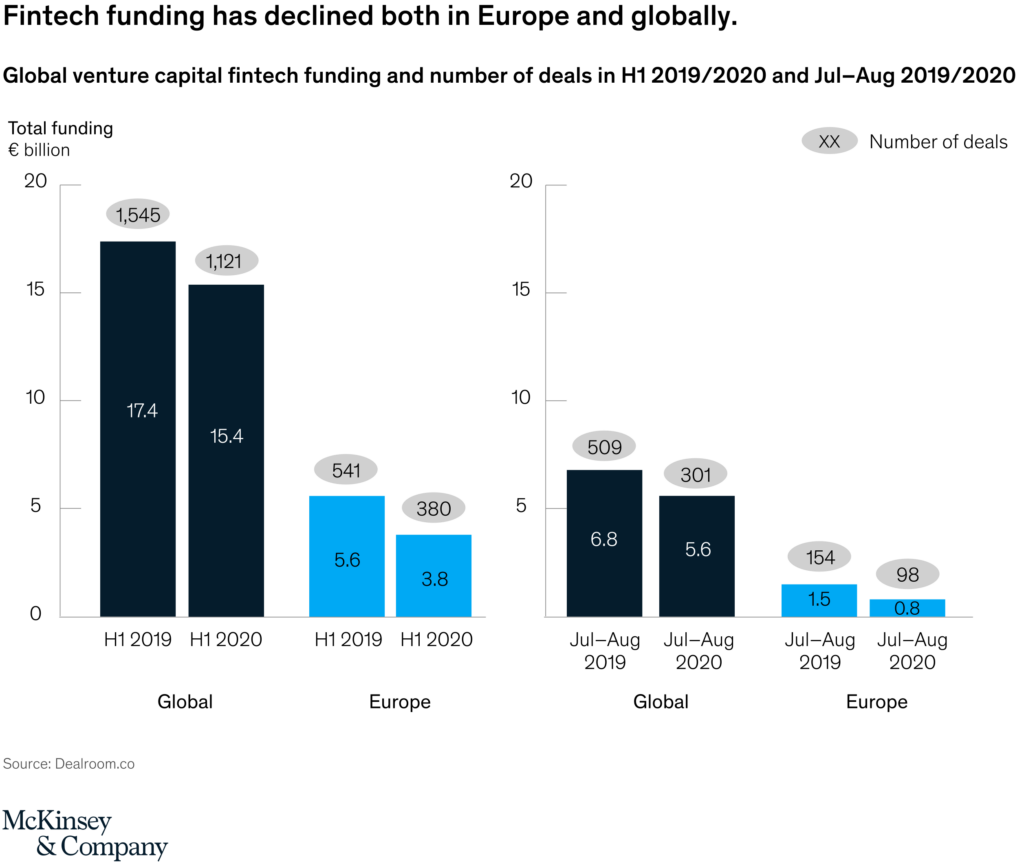

After growing more than 25% a year since 2014, fintech investment dropped by 11% globally and 30% in Europe in H1 2020, compared to the same period in 2019. With fintech funding declining, cash-consumptive fintechs will have to make strategic adjustments and pursue more economically viable paths, McKinsey & Company said in a recent blog post.

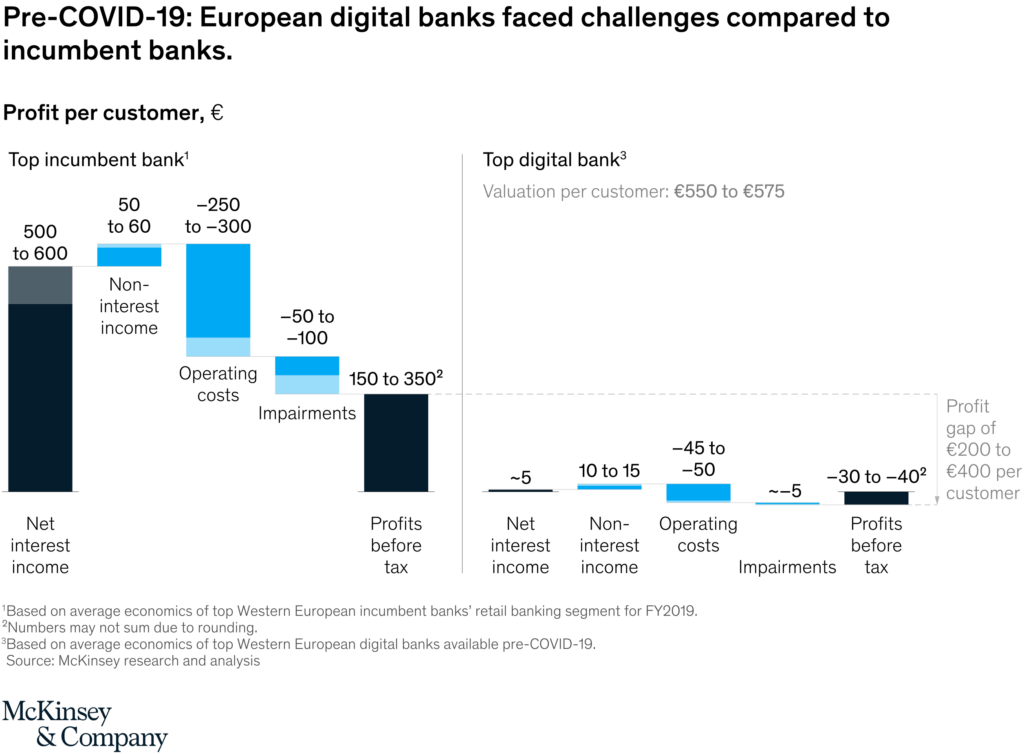

In particular, digital banks that are skewed towards customer acquisition and which require continual investor funding will be put to the test. Pre-COVID-19 already these players faced challenges compared to incumbents but the pandemic is further putting pressure on them to turn a profit.

Pre-COVID-19, loss per customer at top digital banks was between EUR 10 and EUR 60, while top-performing incumbent banks generated EUR 150 and EUR 350 per customer. Now, fintechs’ loss per customer is expected to expand to EUR 20 to EUR 75, while profit per customer at top incumbent banks is expected to drop to EUR 50 – EUR 200, the firm estimates.

Pre-COVID-19, loss per customer at top digital banks was between EUR 10 and EUR 60, while top-performing incumbent banks generated EUR 150 and EUR 350 per customer. Now, fintechs’ loss per customer is expected to expand to EUR 20 to EUR 75, while profit per customer at top incumbent banks is expected to drop to EUR 50 – EUR 200, the firm estimates.

Monoline businesses like peer-to-peer (P2P) lending and marketplace financing too have been negatively impacted by the pandemic, having to face challenges such as higher credit risk, and new regulatory obligations like payment holidays.

McKinsey cited the case of RateSetter, one of the UK’s largest P2P lending platform, which had to slash interest payouts by 50% earlier this year in anticipation of a wave of defaults under COVID-19.

The alternative lender said in May 2020 that 6% of borrowers had requested a payment freeze and as a result, it was increasing its projected loan losses. The saving from cutting interest rates would be diverted to prop up its Provision Fund, which provides a financial safety net for investors in the face of a default, RateSetter said.

Finally, business-to-business (B2B) fintechs will have to deal with an increasingly challenging selling environments, McKinsey said, though those that help financial institutions digitize, automate and reduce their costs will likely continue to get attention and win sales.

Adapting to the new normal

Many fintechs will have to quit “burning money unsustainably” and “spending themselves out of business,” This will require them to cut international expansions plans, business lines and initiatives, and “focus their energies and capital on areas … with long-term potential,” McKinsey said.

Some players will need to readjust their strategies to these new market conditions and changing customer behaviors. This could mean expanding their offering by for example helping governments provide fiscal reliefs and COVID-19 programs. This could also mean expanding into other markets and segments.

Business-to-consumer (B2C) fintechs like digital banks could consider white-labelling their technology platforms and digital capabilities, while B2B fintechs could reconsider their pricing structure and shift to a usage-based model to attract cost-conscious buyers, McKinsey said.

Though COVID-19 might require several fintechs to recalibrate their focus, the crisis-fueled shift to digital channels will nevertheless continue to bring plenty of opportunities by accelerating demand for digital banking and digital transactions.

McKinsey’s Financial Decision Maker Pulse Survey, which was run in early April 2020, found that as many of 80% of consumers in Western Europe prefer handling everyday financial transactions digitally. Between 5 to 20% of consumers in these markets expect to do more digital banking in the future.

McKinsey’s Financial Decision Maker Pulse Survey, which was run in early April 2020, found that as many of 80% of consumers in Western Europe prefer handling everyday financial transactions digitally. Between 5 to 20% of consumers in these markets expect to do more digital banking in the future.

These findings coincide with results from a study conducted earlier this year by Goodwin, which found that 39% of banks and financial institutions around the world are making fintech adoption a high priority, highlighting the global demand for a more advanced financial landscape.

European organizations were found to be more dedicated than their US counterparts to fintech adoption and investment, allocating between 11% and 30% of their profits to fintech.

Further consolidation

These new economics induced by COVID-19 will likely prompt a wave of consolation, McKinsey said. With fintech valuations falling steeply across the board, incumbent banks and corporates will take that opportunity to enter new areas and gain access to talent and technology.

French financial services group Societe Generale said in June that it was acquiring French fintech startup Shine to develop its offer for business and micro-enterprise clients. Shine had been developing a challenger bank for freelancers and small companies in France.

Acquisitions will also continue amongst fintechs as players look to offer a broader customer value proposition and fill monetization gaps in their business models. With the market further consolidating, competition weakening or simply going out of business, mature and successful fintechs will benefit the most and will continue to attract capital, McKinsey said.

In March, Stockholm-based open banking startup Tink announced that it had acquired Madrid-based Eurobits, a provider of account aggregation services serving over 50 banks and fintechs including BBVA and Santander. Tink said the deal would allow it to continue expanding across Europe and will complement its platform.

The post McKinsey: COVID-19 Pandemic Shakes Up European Fintech Landscape appeared first on Fintech Schweiz Digital Finance News - FintechNewsCH.

Comments